CBDT Notifies Cost Inflation Index (CII) for FY 2026–27: Key Impact on Capital Gains

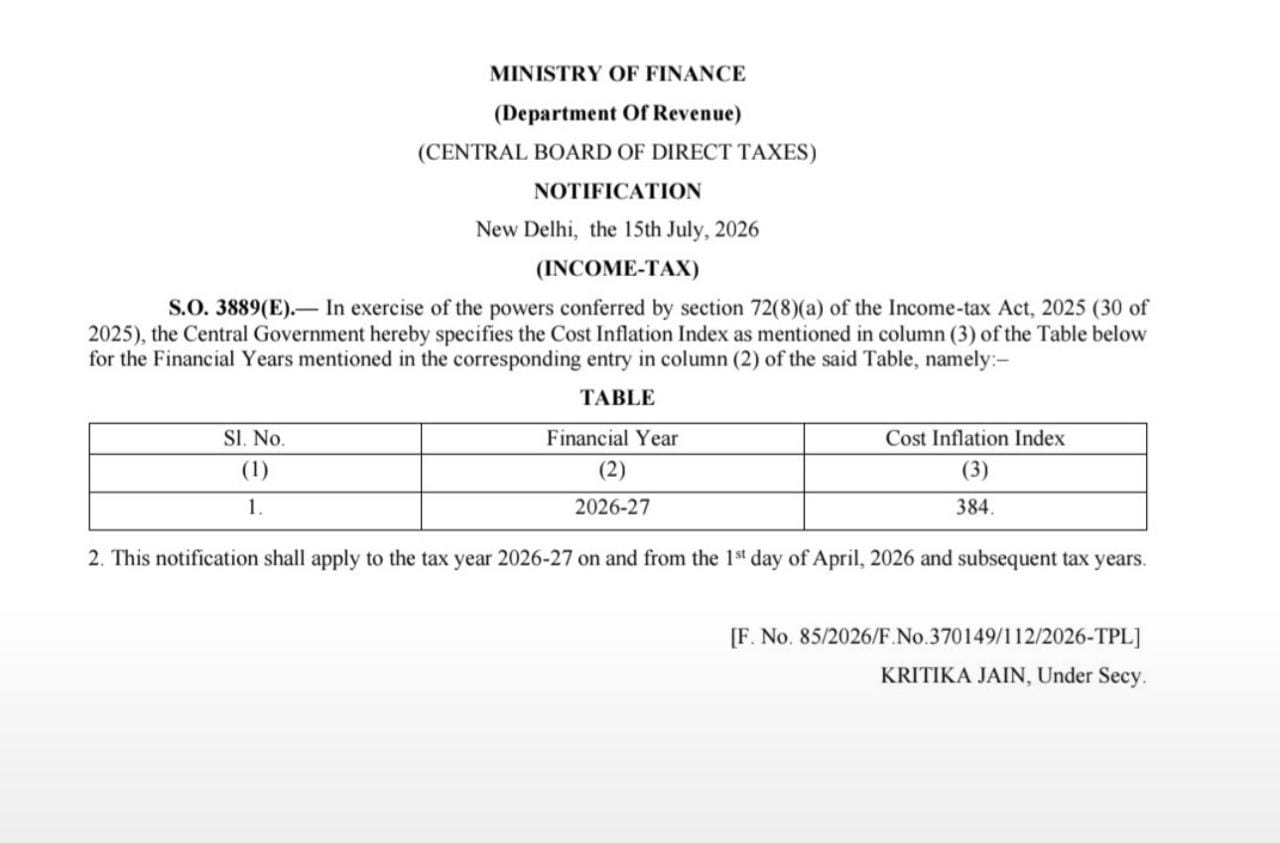

The Central Board of Direct Taxes (CBDT) has officially notified the Cost Inflation Index (CII) for the Financial Year (FY) 2026–27 (corresponding to Assessment Year 2027–28). Vide notification S.O. 3889(E) dated 15th July, 2026, the government has specified the new index value to help taxpayers adjust the purchase price of long-term assets against inflation.

The Key Highlight

According to the official notification issued by the Ministry of Finance, the index number for the current financial year has been set at:

Financial Year: 2026–27

Cost Inflation Index (CII): 384

Effective Date: 1st April, 2026

This is an increase from the previous financial year's (FY 2025–26) index value of 376.

What is the Cost Inflation Index (CII)?

The Cost Inflation Index is a tool used by tax authorities to estimate the annual increase in an asset's price due to inflation. When you sell a long-term capital asset, your nominal profits might look high purely because of the general price rise over the years.

By applying the CII, you can calculate the Indexed Cost of Acquisition. This adjusts the original purchase price upward to reflect real-world inflation, effectively lowering your taxable Long-Term Capital Gains (LTCG) and reducing your overall tax outgo.

Current Relevance of CII Post-Budget Rules

While the notification of the CII remains an annual tradition, its application changed significantly following structural tax amendments.

Important Note on Indexation Benefits:

For most asset classes, long-term capital gains are taxed at a flat rate of 12.5% without indexation. However, a critical grandfathering relief remains:

For Land or Buildings: Resident individuals and Hindu Undivided Families (HUFs) who acquired real estate before July 23, 2024, still have the choice to compute their tax liability at either 20% with indexation or 12.5% without indexation, paying whichever amount is lower.

For taxpayers looking to claim the 20% tax rate option on their older property investments, this new index value of 384 will be crucial for computing the exact tax savings for any transactions happening in FY 2026–27.

Conclusion

The notification of the CII at 384 provides clarity for individuals aligning their tax planning for property sales in the ongoing financial year. If you are planning to sell real estate that qualifies for grandfathered indexation benefits, make sure to use this new index value to evaluate your options accurately.

Have Questions? We're Here to Help

Get expert advice from NEHA K ARORA & CO. Reach out to discuss your requirements.